Businesses Anticipate Unprecedented Rate of Change in 2024, New Accenture ‘Pulse of Change Index’ Shows

Fueled by Generative AI Advances, Technology Leaps from No. 6 to No. 1 Cause of Business Disruption in One Year, According to Key Indicators

While Optimistic, C-Suite Leaders Question Their Readiness to Respond.

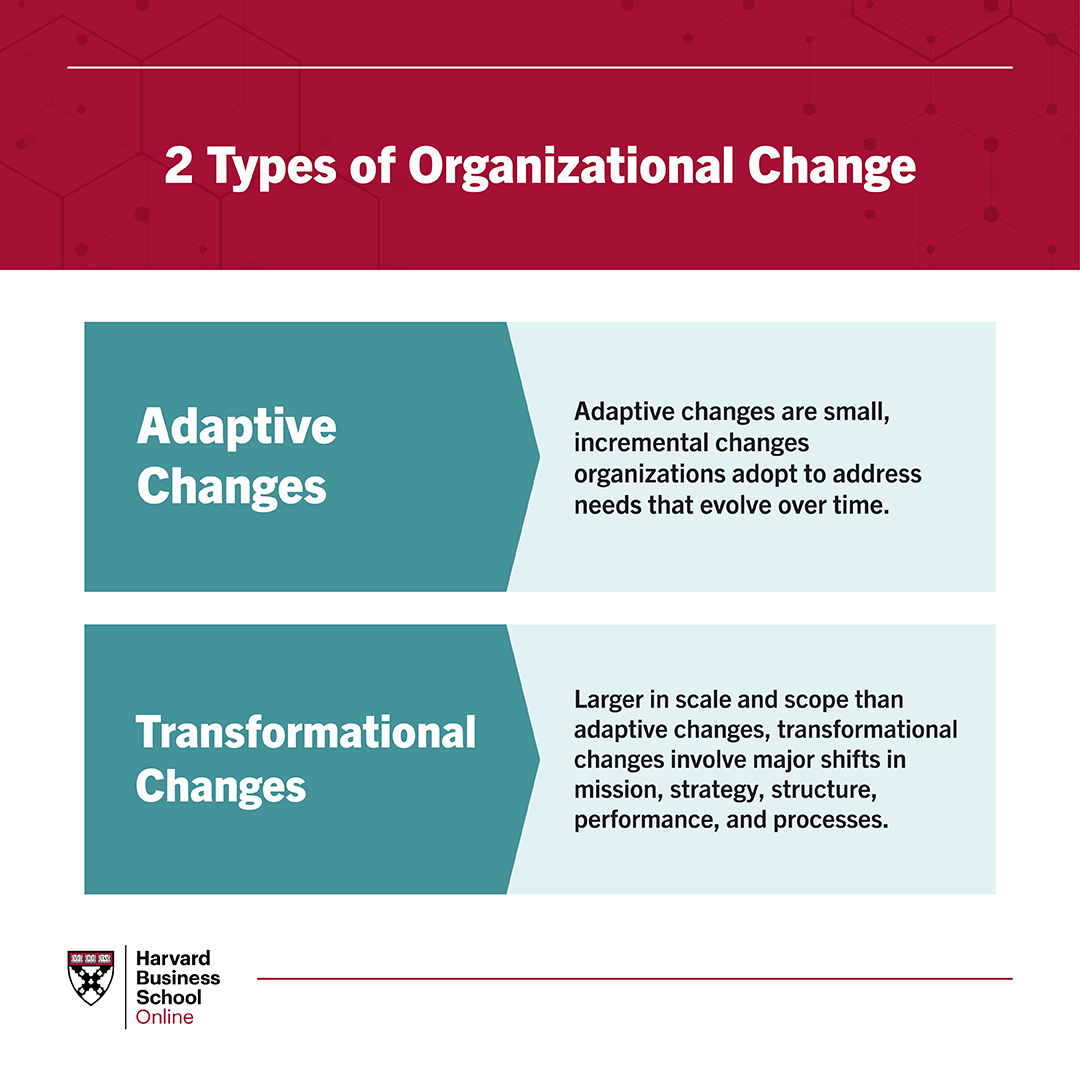

Image credits: https://online.hbs.edu/blog/post/organizational-change-management

The rate of success in an organization is determined by the amount of adaptability of business managers in a thriving environment. The business environment is constantly evolving in response to various business stimuli. In an environment, where change is constant, understanding the Budget Manager’s handbook becomes quintessential in laying the foundations of success.

Mastering the Art of Budgeting

Succeeding as a manager requires a robust set of business skills. In addition to knowing how to navigate key processes like change management and decision-making, managers need an intuitive understanding of finance to drive performance and create value within their organization.

One of the most important finance skills for managers to master is budgeting, or the process of preparing and overseeing a financial plan that estimates income and expenses over a defined period.

Before delving into how you can more effectively budget and improve your management skills, here’s a look at how managers leverage budgets.

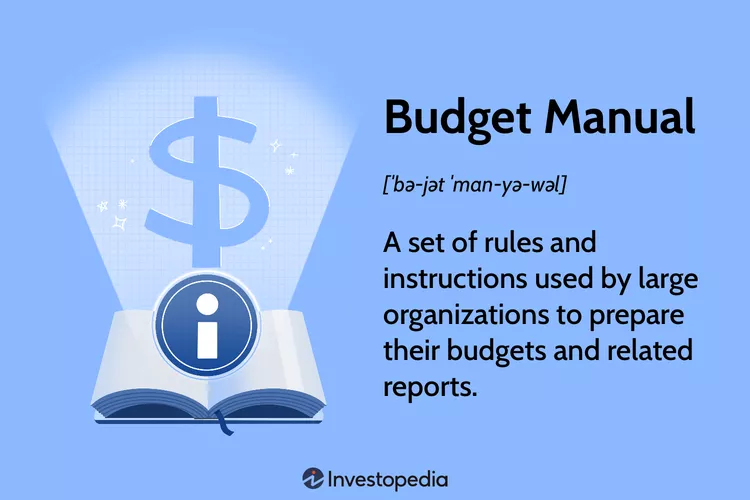

What is the Budget Manager’s Handbook?

Budgeting is a critical financial management tool that enables managers to plan, allocate resources, and track performance. Effective budgeting empowers managers to make informed decisions, align activities with organizational goals, and ensure financial sustainability.

Budgets serve as a roadmap for achieving organizational objectives by outlining the financial resources required for various activities. They provide a basis for monitoring and controlling financial activities, helping managers identify variances and take corrective actions.

Budgeting for Managers

Purpose of Budgeting

Planning: Budgets serve as a roadmap for achieving organizational objectives by outlining the financial resources required for various activities.

Control: Budgets provide a basis for monitoring and controlling financial activities, helping managers identify variances and take corrective actions.

Types of Budgets

Operating Budgets: Focus on day-to-day operational expenses such as sales, production, and administrative costs.

Capital Budgets: Address long-term investments in assets like machinery, equipment, and infrastructure.

Cash Budgets: Project cash inflows and outflows, aiding in liquidity management.

Master Budgets: Comprehensive plans that integrate operating, capital, and financial budgets.

Preparation of Budget

Budgeting Process

- Identification of Goals: Define organizational goals and objectives to guide the budgeting process.

- Data Collection: Gather relevant historical data, market trends, and input from various departments.

- Budget Formulation: Develop detailed budgets for revenue, expenses, and investments based on organizational priorities.

- Review and Approval: Present the budget to relevant stakeholders for review and approval.

HOW MANAGERS USE BUDGETS

At its most basic level, a budget ensures that a team or department has the resources needed to achieve its goals. For managers, the budget serves as a vital tool for:

- Communicating expectations and goals to stakeholders

- Mobilizing teams and departments around organizational objectives

- Assessing group and individual performance

- Gaining insight into an organization’s financial health

- Allocating resources strategically and appropriately

Budgeting within large organizations is an extremely complex task. Financial analysts must make assumptions about what the future will look like based on past data. This means that even the best budgeting process is subject to considerable inaccuracies. Then, as the year progresses, each group is held to a predefined budget, which may become inadequate due to changing conditions.

What is budget management in project management?

Project budget management is the process of estimating the resources you need, setting limits accordingly, and managing spending throughout a project. Most of the time, this process happens in four parts.

Define your budget. During this phase, you forecast your needs, identify your resources, and use that information to set your budget.

Get approval from stakeholders. Most of the time, you must present your plan to decision-makers before you get the resources you need.

Control spending as the project progresses. This includes managing timelines because labor costs are one of your biggest expenses.

Update the budget when things change. A delay at one step might mean that you need more resources later to deliver on time. You may also find that you estimated more expenses than you needed, and updating your budget frees up funds for other projects.

Methodologies and Types

There are various budgeting methods are available for managers to choose from, depending on the organization’s goals, industry, and specific needs. Each method has its advantages and disadvantages. Here are some common methods of budgeting for managers:

Incremental Budgeting:

Overview: Incremental budgeting involves making adjustments to the previous period’s budget, often by applying a percentage increase or decrease.

Advantages: Simple, quick, and easy to implement. Provides stability and predictability.

Disadvantages: Tends to perpetuate past inefficiencies. May not account for changing business conditions.

Zero-Based Budgeting (ZBB):

Overview: ZBB requires justifying every budgeted expense from scratch, without relying on historical budgets.

Advantages: Encourages cost efficiency and a thorough examination of each expense. Forces prioritization.

Disadvantages: Time-consuming and resource-intensive. May be challenging to implement in organizations with a long history of incremental budgeting.

Activity-Based Budgeting (ABB):

Overview: ABB links budgeting to specific activities and their costs. It focuses on the relationship between activities and resource requirements.

Advantages: Aligns budgeting with organizational activities. Enhances cost transparency and resource allocation.

Disadvantages: Requires a detailed understanding of activities and their associated costs. Implementation can be complex.

Flexible Budgeting:

Overview: A flexible budget allows for adjustments to budgeted figures based on changes in business conditions or activity levels.

Advantages: Adaptable to unforeseen circumstances. Supports real-time decision-making.

Disadvantages: Requires continuous monitoring and adjustments. May be more complex than traditional static budgets.

Rolling Budgets:

Overview: Rolling budgets involve continuously updating the budget by adding a new budget period as the current one expires.

Advantages: Encourages ongoing planning and adaptability. Aligns with changing business environments.

Disadvantages: Requires constant attention and updates. May be resource-intensive.

Priority-Based Budgeting:

Overview: Focuses on prioritizing budget allocations based on the organization’s strategic priorities.

Advantages: Ensures that resources are directed to high-priority areas. Aligns budgeting with strategic goals.

Disadvantages: Requires a clear understanding of strategic priorities. May lead to difficult decisions on resource allocation.

Kaizen Budgeting:

Overview: Kaizen budgeting involves continuous improvement by setting incremental improvement targets.

Advantages: Fosters a culture of continuous improvement. Encourages efficiency gains over time.

Disadvantages: May not be suitable for all types of organizations. Requires a commitment to ongoing improvement.

Participative Budgeting:

Overview: Involves input from various levels of the organization, encouraging collaboration and buy-in from employees.

Advantages: Enhances employee engagement and accountability. Draws on the expertise of those closest to the operations.

Disadvantages: Can be time-consuming. This may result in budgetary negotiations that prioritize short-term interests.

When choosing a budgeting method, managers should consider the organization’s culture, management style, and the nature of its operations. A combination of budgeting methods or a customized approach that suits the organization’s unique needs may also be appropriate.

References

Mastering the Art of Budgeting: A Comprehensive Guide for Businesses. (2023, April 4). Wafeq. https://www.wafeq.com/en/learn-accounting/managerial-accounting/mastering-the-art-of-budgeting:-a-comprehensive-guide-for-businesses

6 Budgeting Tips for Managers | HBS Online. (2020, April 23). Business Insights Blog. https://online.hbs.edu/blog/post/budgeting-for-managers