Introduction

The Economies are facing major challenges of revitalization of the ecosystem of banking culture. The surveys conducted by various analytical firms draw key benefits of Open Banking infrastructure. It has set the pace for transformation and evolution in a systematic and organised manner. The posing challenges to the culturing imbibing the system indicates three aspects. These include functioning of banks, reasons for optimization, and option of catalytic activity to research and innovation.

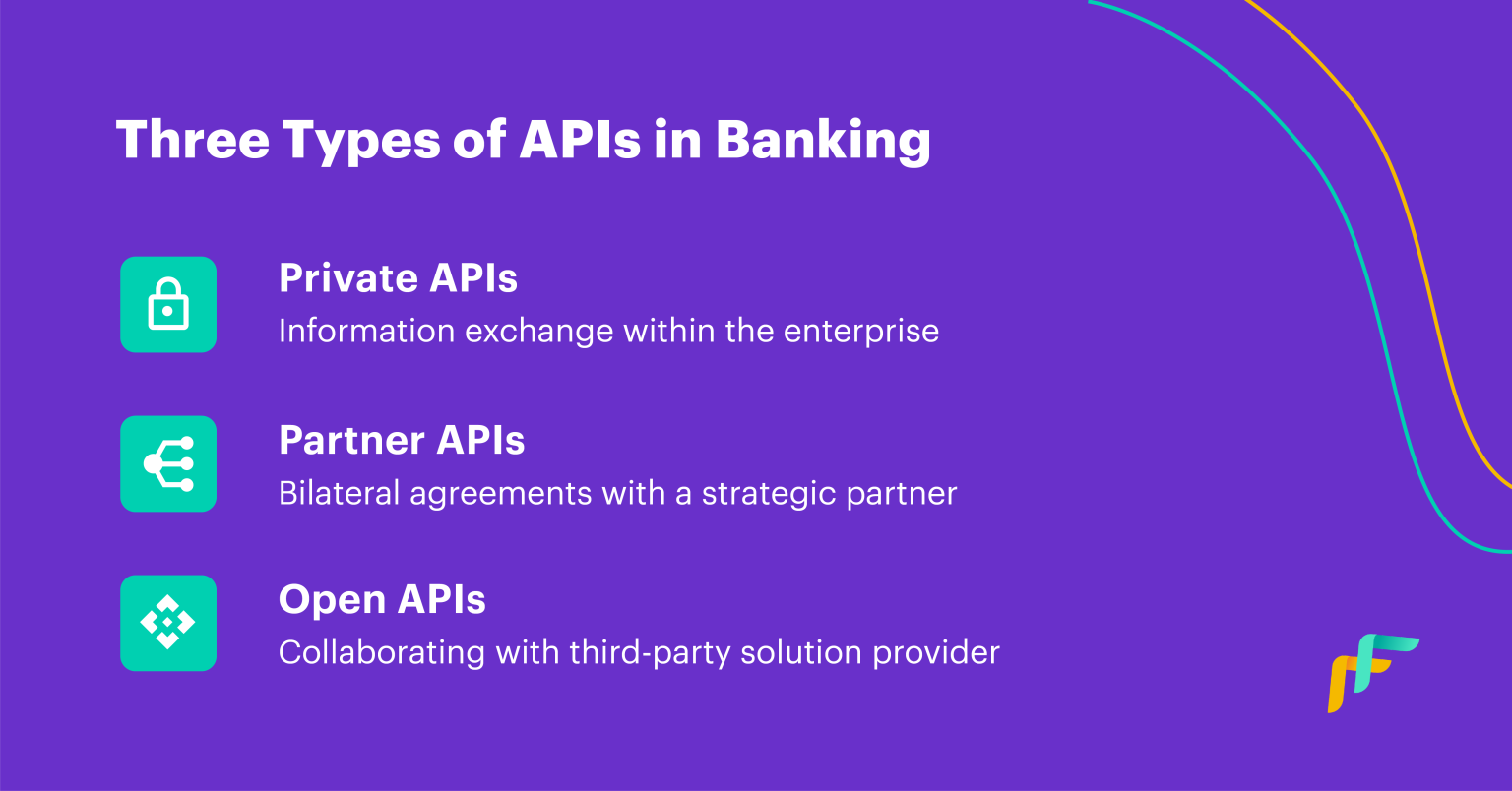

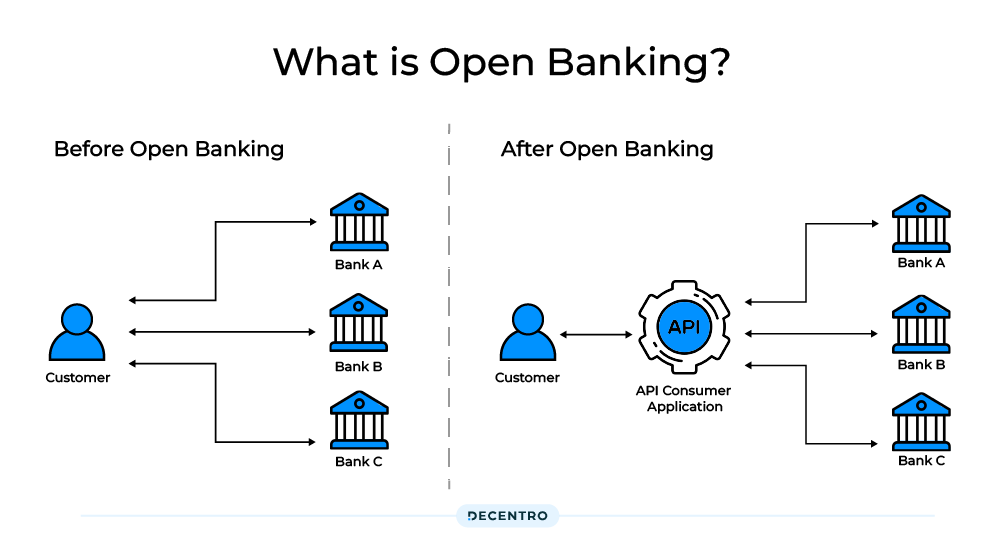

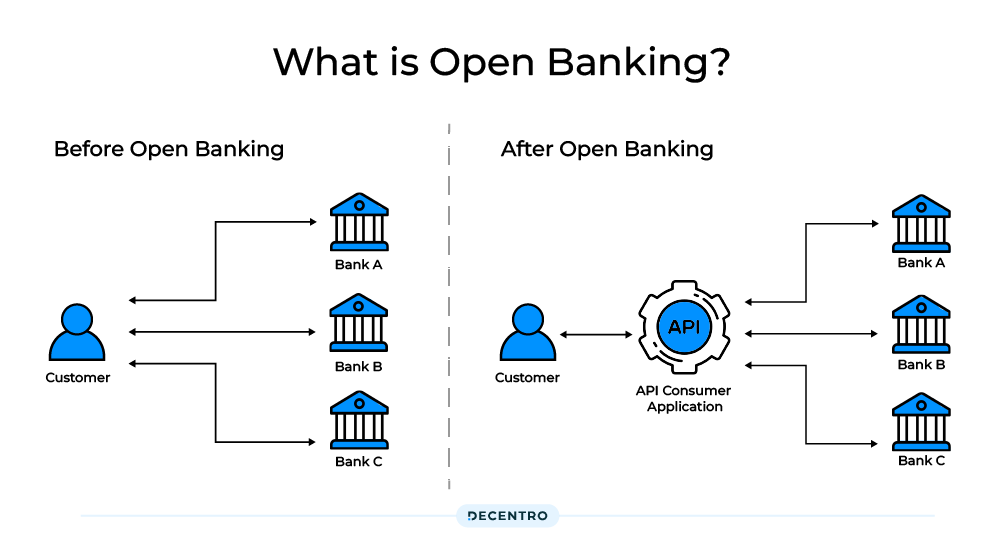

What is Open Banking?

Open Banking functions as an intermediary between Banks and third party service providers by the means of usage of application programming interfaces. This permeates sharing of financial data between the two parties involved in the transaction.

Open Banking is the Future

The question arises, aren’t banking eco-culture self-sufficient enough to maintain databases for storage of Consumer’s data. The answer is no. With the growing demand of Data analytics to handle cumbersome. It’s not feasible to rely on traditional digital banking means to store and consume data. This is where open Banking comes to rescue. But, can all afford it. In reality, the major institutions have been able to pave pathway to unlocking the promise of open Banking market infrastructure.

How Open banking works?

The APIs in open Banking infrastructure majorly provide financial data and services with third parties who specialise in technology. Adyen is a payment processing company that offers open banking APIs for account verification and payments processing. Fena is an app that allows users to transfer money between accounts quickly and easily.

Unlocking the Gates of Open Banking

The developed economies have begun their open banking experiments, yet the majority hold little or no knowledge in the realm of open banking. The buzzword in the realm of fintech, banking has often faced blank stares when brought in business rooms despite its presence for over a decade.

Image Credits: https://decentro.tech/blog/wp-content/uploads/before_after.png

{kind=link}

Open Banking: Need of the hour

Despite the unawareness, the question arises what is the need of open banking. The implications and further complications reaps various benefits of streamlining revenues by bringing more customised and contextual banking experience. The economies are facing a shortage of software aiding the transmission and storage of data around the consumer base. the posing question revolves around evolution acting as posing demand by regulatory standards of various authorities. This further broadens the horizon of permissions acknowledging the risk of breach of consumers’s data. The infrastructure and ecosystem permeate the digital exchange of financial data.

Customer’s Reliance

Customers are ready to trade personal data in exchange for a customised experience. In fact, providing real value in exchange for customer data can increase loyalty and trust. Interestingly, 48% of customers expect banks to provide product information related to their actions on the app/website. Furthermore, customers are looking for accessibility. Surveys by PwC found that 15% of banking customers preferred to do banking by mobile. These customers expect a full range of banking and financial services on these apps. These services can range from fully automated dashboards to real-time transaction status updates.

Steps in Unlocking the Promise of Open Banking Market Infrastructure

- Optimization of Digital Sales.

- Scaling Relationship Banking.

- Securing third party distribution.

- Designing Bank wide loyalty programs.

- Owning Journeys for Key Client Segments

Open Banking not only brings out many benefits for end users and fosters innovation within the Fintech sector, but also increases the competition between banks and non-banks. Access to financial data can bring in many new business models within the market. Banks’ role will also change as Open Banking is adopted. It increases the liability of the financial institutions by posing higher security risks to customers’ financial data. It is also known at times for malicious attacks to wipe customer accounts. Hacking and data breaches due to poor security measures have become more of a threat in the advanced world.

Overall, everything comes with its boons and disadvantages. It’s in the best interest of customers to leverage Open Banking services ensuring proper security practices are being followed.

The Change in Banking Infrastructure

Here, banks need to tap into the power of open banking API to collaborate with fintech players. In such a scenario, the customer can get access to a unified solution and the bank can provide customer satisfaction. Furthermore, banks can collaborate with fintech companies to further provide for a customer’s focused interest. This kind of competition can be termed a ‘market force’. A lot of banks in India, the US, China and Singapore are investing in open banking APIs because of such forces. However, at the end of the day, it does not matter if the growth is driven by market forces or government regulations. After all, the end result for both kinds of economies is higher innovation and price transparency.

Open Banking Case Study: In India

API-based banking products and services are already gaining traction in the market. Major countries have government regulations to enforce open banking. These regulatory frameworks allow third parties to access customer-permission data. These third parties are required to gain licences. The banks have to implement data privacy and consent agreements.

State of API banking platforms in India

In India, the growth of open banking and API is largely due to market forces. Intermediaries licensed as Non-Banking Financial Companies (NBFC) are responsible for customer consent management.

Moreover, an Account Aggregator (AA) is a licensed entity that connects a Financial Information Provider (FIP) (Eg. Banks) to Financial Information User (FIU). AA connects these two entities through APIs.

The transfer of any personal customer data is regulated strictly in India.

There are appropriate agreements between the customer, the AA and the financial information providers. Moreover, data cannot be stored or used by aggregators for any other purpose. All AAs have to keep explicit data security policies and customer grievance redressal systems in place.

Open Banking Case Study: In United Kingdom

The UK started introducing an Open Banking Standard in 2016 to make the banking sector work harder for the benefit of consumers. The implementation of the standard was guided by recommendations from the Open Banking Working Group, made up of banks and industry groups and co-chaired by the Open Data Institute and Barclays. It had a focus on how data could be used to “help people to transact, save, borrow, lend and invest their money”.

Open Banking: Banking Initiatives

The YES Bank partnered with fintech startups with an accelerator program. Moreover, it has created a chat-based payment service. Axis Bank has established an accelerator program, an in-house incubator program and even a social networking space for startups. State Bank of India enables customers to make transactions through their fingerprints and Aadhar number. This is possible through Aadhaar Enabled Payment System (AEPS)

Conclusion

Open banking APIs have a huge role in fueling fintech growth. In fact, because of this, a lot of fintech players offering customer-friendly finance solutions have come up. Let’s have a look at some of them here. These fintech players allow merchants and users to invest in other companies. Moreover, they provide lending services. Similarly, some investors or crowdfunding companies may invest in other businesses in return for sharesThe investment solution market companies may help clients with informed investment decisions and provide market data. These companies help customers with managing personal finance like tax filing, financial advice etc.

References

^ Premchand, A.; Choudhry, A. (February 2018). “Open Banking & APIs for Transformation in Banking”. 2018 International Conference on Communication, Computing and Internet of Things (IC3IoT). pp. 25–29. doi:10.1109/IC3IoT.2018.8668107. ISBN 978-1-5386-2459-3. S2CID 84185109. Archived from the original on 4 April 2023. Retrieved 15 May 2023.

^ Open Banking Working Group. “The Open Banking Standard” (PDF). HM Treasury. Archived (PDF) from the original on 18 April 2017. Retrieved 18 April 2017.

^ Brodsky, Laura; Oakes, Liz (September 2017). “Data sharing and open banking”. McKinsey & Company. Archived from the original on 8 November 2017. Retrieved 7 November 2017.

^ “When Open Innovation comes to banking – BNP Paribas”. BNP Paribas. Archived from the original on 27 January 2021. Retrieved 29 October 2020.