Introduction

In an era of automation taking over across all spheres of life. It’s difficult to imagine life without e-wallets and banks in a mobile application! The question arises, despite the ease and comfort. Are the consumers satisfied and are having pleasure out of their banking experience? Also, in the decade where Machine learning and Artificial intelligence are taking the lead. How much digitisation is necessary for banks? Is it a mere desire with less economic efficiency with a large corpus spent on research and development.

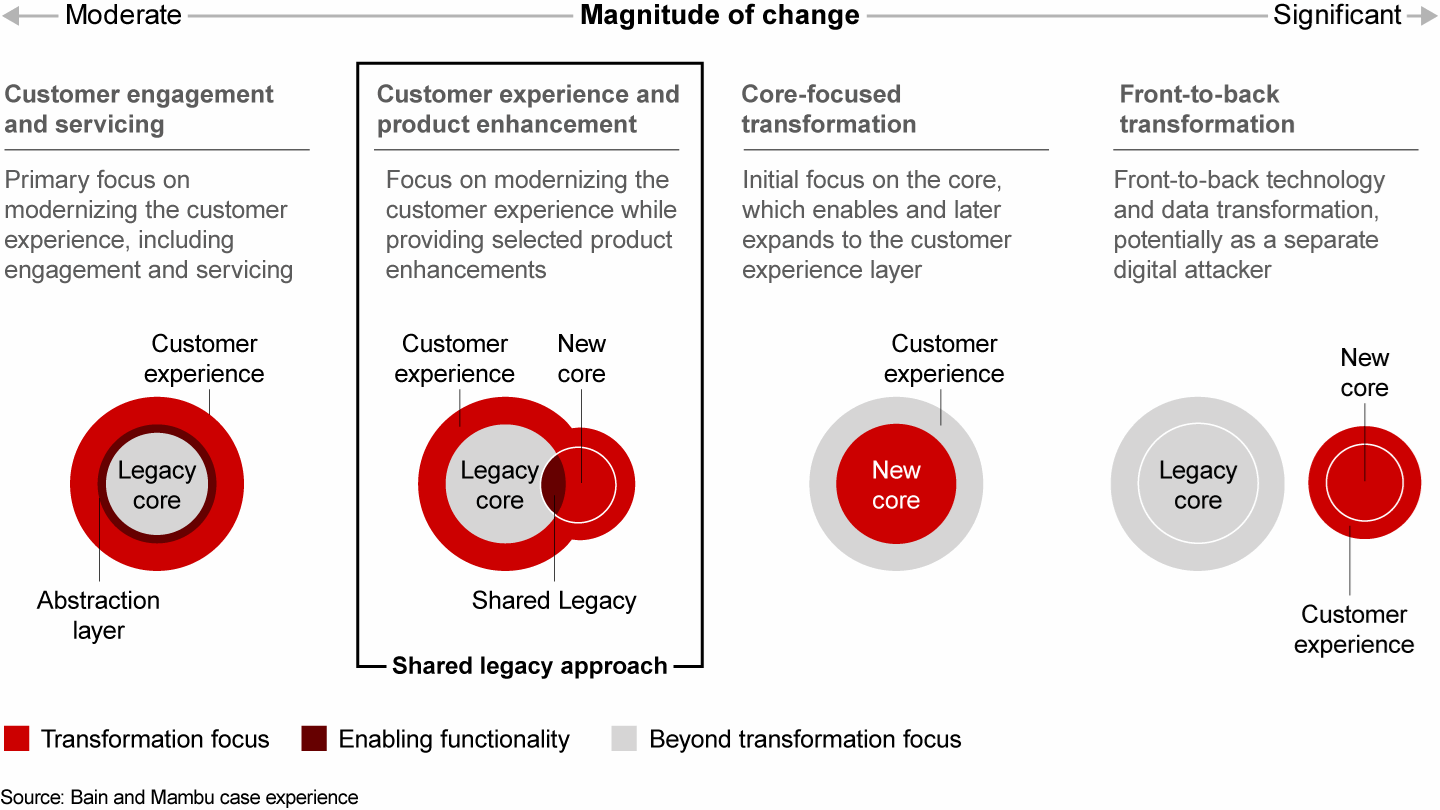

The Bain Report quotes,

Today’s customers, especially millennials and Gen Z, expect digital, personalised experiences. 71% of millennials would rather go to the dentist than listen to what banks have to offer.

Digital channels better serve these preferences.

Unveiling Core Banking Strategies for Growth

The core banking strategies are contrasting to the basic strategies behind fundamental banking services.

These primary services include online banking, mobile banking, ATMs, internet banking and Chatbots. They revolve around web services, cash withdrawals and deposits, and AI customer services. The primary banking strategies for growth can be described as follows:

- By excelling at personalization and customer centricity, neobanks and fintechs are gaining an edge on traditional banks.

- To compete—and rapidly deliver and scale customer-centric propositions—incumbents can take an agile approach rooted in business objectives.

- Though there are several paths to technology transformation, a shared legacy approach—combining cloud-native digital platforms with banks’ existing digital capabilities—helps banks avoid a full reboot.

What’s contrasting, is major banks follow strategies which revolve around these services. Despite, the banks need to look beyond digital.The surveys around customer satisfaction conducted among US banking consumers reveals around eighty percent cent of the population cater to digitisation in banking. This indicates, there is a level of saturation among masses around digital banking.

Beyond Digital: Unveiling Strategies for Growth in Banking

Growth strategies other than basic banking facilities revolve around few fundamental parameters –

1. Inclinations of Consumer’s Base

2. Intensity of penetration of E-Banking services

3. Amount of Economic efficiency among various strategies.

Other than primaeval services, aspects like research and innovation as well as regulatory standards play a crucial role. What also enhances the banking experience is the rivalry. The competition offered by Fintech, and competitor services by various banks. Technological advances in the fields of Artificial Intelligence, Blockchain and Cybersecurity.

Understanding the sphere of Digital Banking

What works in E-Banking services is cost efficiency and convenience offered on both sides. Gone are those days of licking stamps, signing checks and standing in the queues for hours. Still, has it offered substantial revenue growth and increased the savings account in the sphere of Digital Banking. Has it made lives better, made banking more penetrated in funnel shape for all spheres of life. Yet it has offered few challenges in areas of security, accessibility in terms of financial literacy and challenges in user’s experience.

Design for customers, not banks: A sound understanding of the market, including its most profitable segments, customer preferences, and how the competition stacks up, will reveal the biggest growth opportunities.

Plan for realistic outcomes: After establishing a viable business case, de-risk execution by identifying and mitigating potential roadblocks before the actual kickoff.

Build demand as well as products: Observe how leading banks have brought new products to market profitably and sustainably. Apply a test-and-learn approach and iterate through rapid customer feedback cycles.

Use scale as an advantage: A larger customer base means more feedback as well as more resources to develop and deliver value to customers and markets.

Banking Growth Strategies Beyond Digital

- Increase Bank Profitability & Grow Your Commercial Loan Portfolio with a Customizable Debt Collection Technology Product

- Intelligent Banking Solutions pioneered customizable debt collection technology to solve the critical challenges of increasing bank profitability, growing loan volume, and reducing risk for all financial institutions.

- Integrate your current banking business policies, compliance strategy definitions and leverage full or collector action initiated work flows.

- Efficient workflows and automated outreach allow for earlier and more frequent debtor communication.

- Provides additional communication channels (pre-recorded voicemail, SMS, email)

- Expands the collection period beyond the daily hours that collectors are typically in the office

- Increases the probability of debtor contact and subsequent follow-through with payment

- Reminds borrowers of payment deadlines and holds them accountable.

- The scalable, user-friendly software allows for unlimited collector assignments, and quickly adapts to enforce changes to the ever-changing economic environment, policies and regulations that affect your debt collection and recovery strategy.

- Creation of a robust debt collection system enables your collection staff to execute your financial institution’s collections strategy.

- Risk mitigation with stringent debt collection processes and consistent follow through, as a single compliance error

Case Studies

Full Scale Digital Banking Experience

National Australia Bank (NAB) launched UBank, a branchless Direct Retail Bank in 2008. It focuses on customer service and user-friendly front-end applications so that customers can always engage

easily with the bank. It aims to offer real lifestyle banking, rather than a series of discrete transactions. UBank has introduced several innovative products, including People Like U. People Like U is a social

comparison tool that allows customers to see the anonymized spending and budgeting data of their peers. RoboChat is a Robo-advisory application that can grant loan approvals in minutes. UBank achieved its two-year customer acquisition target within its first six months, signing up as many as 10,000 customers a month. It reduced a two-day customer on-boarding process for deposit accounts down to just five minutes. UBank has been the key driver behind NAB’s expansion of its market share for

deposits.

Valuable lessons

Traditional and virtual banks thus need to develop the ability to:

- Respond with speed to new market developments.

- Incorporate new products and processes rapidly onto banking platforms.

- Offer more choices to the end-user for their profitability objectives.

- Easily connect with 3rd party products to offer a hyper-personalised service for the customer.

A Conclusive Analysis

Looking beyond Digital Banking: Analytical and Data Driven Analysis

The surveys conducted by various analytical firms draw key benefits. These benefits reap on data analysis providing insights on lessons for Gen Z banking experience. The Banking Growth Strategies reaping on Profitability, Scalability, and Revenues. The strategies development has been cohesively around two parameters – one is of business ecosystem, banking experience in the market, technology and connectivity.

Digital Banking reaped various benefits due to the wave of digitization. The result was change in compliance standards allowing fintechs and virtual banking experience. But, this posed a bigger challenge of how the growth strategies alter order to grow, replicate and generate further revenues.

References

Team, C. (2024, January 24). Banking in the Tech Age: Unveiling Key Strategies for 2024 with Satyam Agrawal. Credable. https://www.credable.in/insights-by-credable/business-insights/banking-in-the-tech-age-unveiling-key-strategies-for-2024-with-satyam-agrawal/

Banks’ new growth path: from the customer to the cloud. (n.d.). Bain. https://www.bain.com/how-we-help/banks-new-growth-path-from-customer-to-cloud/

Marous, J. (2022, April 22). Measuring and reducing friction in account opening. The Financial Brand. https://thefinancialbrand.com/56792/bank_account-opening-application-improvement-scoring/

PricewaterhouseCoopers. (n.d.). Financial services. PwC. https://www.pwc.com/gx/en/industries/financial-services/banking-capital-markets/banking-2020.html

Khanna, S., & Martins, H. (2018, April 13). Six digital growth strategies for banks. McKinsey & Company. https://www.mckinsey.com/capabilities/mckinsey-digital/our-insights/six-digital-growth-strategies-for-banks