Source: Voldico.com

Originally, insurance was developed to help individuals and businesses manage risk and mitigate the impact of unpredictable events. Today, there’s a plethora of insurance options available, all with the same underlying purpose but often in a complex and rapidly changing landscape.

Trust plays a crucial role in the insurance industry. For customers, it involves relinquishing control, relying on expertise, and feeling secure in their decisions. Building trust requires a strong partnership between insurers and clients, as a lack of trust can result in subpar performance.

In light of the disruptions caused by COVID-19, companies may find it necessary to move beyond conventional practices and adopt proactive measures rather than simply reacting to events.

Accident Law Group: Should you trust your insurance company?

It’s widely acknowledged that trust, defined as an individual’s confidence in a third party’s future actions, is a fundamental component of the insurance industry. Insurers essentially operate on the foundation of trust, offering promises to pay contingent on future events, often occurring at a distant and unspecified time, such as in life insurance.

For policyholders, evaluating the insurer’s willingness and capability to fulfill these commitments is typically only possible after filing and settling a claim. The insurer’s performance remains partially hidden at the time of policy purchase due to information imbalances. These disparities make it challenging for policyholders to immediately gauge the value of an insurer’s promise to pay. However, factors such as the overall reputation and track record of an insurance company, along with a robust legal and regulatory framework, play crucial roles in building trust with policyholders.

Source: Livelearn.ca

Furthermore, collective trust among policyholders in insurers can be undermined by external factors. For instance, the prolonged period of ultra-low interest rates has diminished confidence levels in certain mature life and health insurance markets.

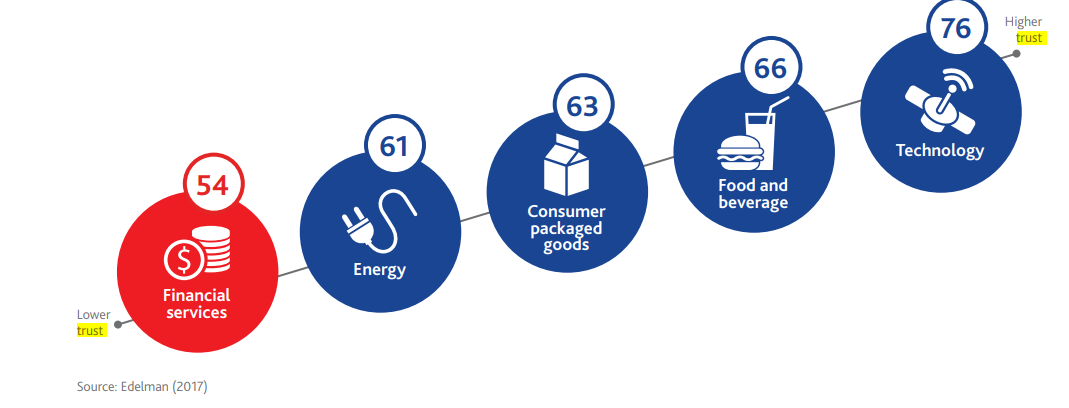

Source: Edelman

Global surveys indicate a significant public trust gap in financial services overall, with insurance being particularly affected compared to industries like energy, consumer goods, food, and technology.

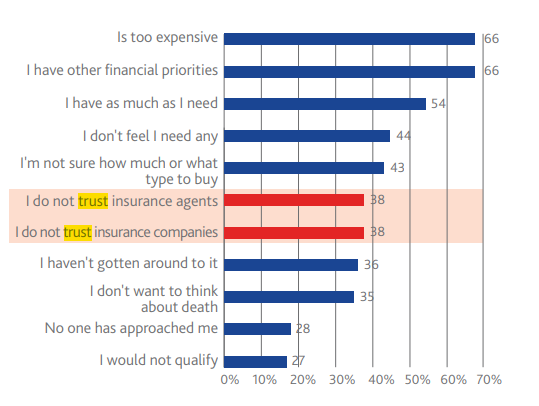

Mistrust is the top reason behind the life insurance protection gap in the U.S.

source: Rozar, Limra (2017)

Determine the problems and underlying reasons

1. Ambiguity in policies

Buyers frequently find themselves unsure about the products they’re purchasing. The Financial Conduct Authority’s report on Smart Consumer Communications criticized the financial industry for its use of confusing jargon and bureaucratic processes, which creates a “fog” for consumers. The FCA emphasized the need for clearer communication, simpler information, and the establishment of trust in firms. Additionally, consumers using digital channels require communications tailored to today’s digitized context.

According to a survey by EY, only 65% of fintech adopters and 52% of non-adopters read the terms and conditions when signing up for a new financial product. Many consumers still prefer the security of face-to-face conversations, posing a significant cost burden for providers.

How are ambiguities in insurance policies resolved?

2. Lack of transparency in pricing

Price comparison sites often present a wide range of quotes for essentially identical products, leading to consumer skepticism. Manan Sagar, Chief Technology Officer EMEIA of Fujitsu UK, highlighted the frustration of receiving significantly higher quotes for renewals without clear explanations. Consumers demand transparency in pricing, such as being informed about factors influencing premium increases based on their driving performance data.

3. Breaches of privacy

Data breaches undermine trust in financial service brands, with insurers sometimes being the perpetrators due to misjudged assumptions about consumer tolerance. Even well-intentioned initiatives can backfire, as seen with Admiral Insurance’s plan to use Facebook posts to analyze user personalities, which was withdrawn due to privacy concerns.

4. Impersonalized products

Consumers seek providers who understand their unique needs, yet many insurance products lack relevance. Whether due to overly broad coverage options, inflexible policies, or difficulty in expressing personal circumstances, personalization in insurance remains underdeveloped among traditional providers.

5. Poor user experience and customer experience

In contrast to the intuitive and refined user interfaces of elite technology companies, insurance lags behind in customer experience. Processes such as onboarding can be lengthy, KYC procedures are intrusive, and policy information is difficult to access online, highlighting a need for improvement in the overall customer experience.

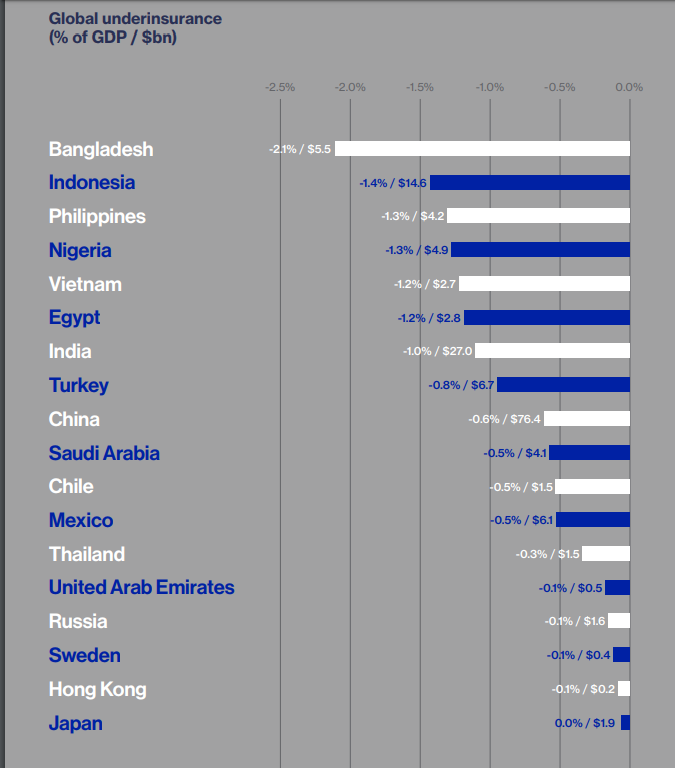

How big is the global protection gap?

The global protection gap is determined by assessing the extent of risk covered by insurance policies annually compared to the expenses incurred by businesses and governments for rebuilding and recovering from major disasters.

The specific figures for each country were unveiled in Lloyd’s report focusing on narrowing the insurance gap.

Bangladesh emerged as the nation with the highest degree of underinsurance, facing a $5.5 billion (£4.34 billion) gap in insurance coverage equivalent to 2.1% of its GDP.

However, several developed countries, such as Turkey, Sweden, and Japan, also featured on Lloyd’s list of the most underinsured markets.

Lloyd’s of London 2018 global underinsurance data (Source: A World At Risk: Closing the Insurance Gap)

Turkey ranked eighth in terms of the protection gap, amounting to $6.7 billion (£5.3 billion) or 0.8% of its GDP.

Japan, one of the countries analyzed by the Geneva Association, faced a protection gap of $1.9 billion (£1.5 billion). However, due to Japan’s substantial GDP, a loss of that magnitude would have such a minor impact on its overall economic activity that Lloyd’s reported the figure as 0% of its GDP.

Obtaining figures for Europe is challenging because the levels of underinsurance relative to countries’ GDP are so low. According to Lloyd’s report, three of the largest insurance markets surveyed by the Geneva Association are not underinsured at all.

The report stated, “Germany, France, and the UK are adequately covered relative to expected losses. Between 2004 and 2017, approximately two-thirds of the losses from natural catastrophes in these countries were recovered through insurance.”

The best possible experience for customers

The most common worries are related to services, although there are also reservations about products. Simpleness, adaptability, and communication are contentious topics. A modern, ideal customer experience would have the following components:

1. Contracts structured with simple, succinct explanations and outlined in a straightforward, easy-to-understand manner.

2. Flexibility in terms and conditions, allowing customers to adjust their coverage to accommodate evolving circumstances over time.

3. Reduced ambiguity to enhance predictability and clarity for customers.

4. Enhanced responsiveness, achieved through shortened response times facilitated by InsureTech initiatives, such as AI-based valuation systems.

5. Segregated or regulated financial advice to ensure impartiality and transparency, distinct from product sales processes.

Reference:

[1]https://www.linkedin.com/pulse/six-reasons-low-trust-insurance-industry-two-theories-gabor-pal/

[2]“Trust in insurance: winning back customers.” FintechOS, 30 July 2020, Accessed 4 April 2024.[3 ]https://www.nsinsurance.com/analysis/the-geneva-association-survey/