As the calendar approaches its final pages, business owners are gearing up for one of the most critical tasks of the year: year-end financial management. Amidst the holiday hustle and bustle, it’s imperative to ensure that your financial house is in order. Much like plotting out your daily tasks, crafting a thorough year-end accounting checklist can be the difference between a smooth transition and a chaotic scramble.

Referred to as “closing the books,” year-end financial management entails a meticulous review, reconciliation, and preparation of all financial transactions and records from the preceding fiscal year. This involves a deep dive into expenses, income, assets, liabilities, equity, and more. The ultimate objective? To compile accurate financial statements that not only provide insights into the company’s financial health but also serve as a roadmap for future decision-making. These statements become the bedrock of the company’s official financial records, guiding strategic planning and investor relations.

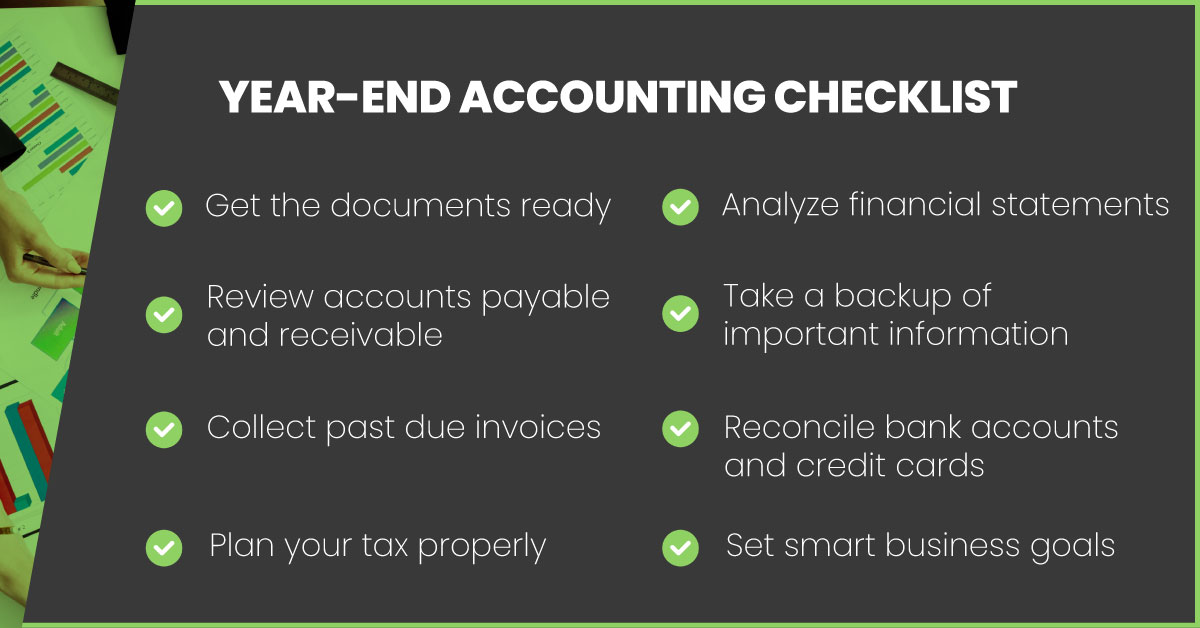

✅ Year-end Accounting Checklist – 8 Steps to Get Your Books Ready for Your Accountant 🤓

Why do we need a year-end Accounting Checklist?

Accountants are known for their busyness, especially as year-end approaches. Even the most seasoned accountants find themselves with their hands full, striving to meet deadlines. Year-end accounting presents a unique challenge due to the multitude of tasks involved – from preparing financial statements to gathering tax documentation. Each task is intricate and often requires a specific sequence. Multiply this complexity across multiple clients, and the potential for chaos becomes evident. Mistakes, inaccuracies, and incomplete processes loom large.

To navigate this complexity, a year-end accounting checklist proves invaluable.

It serves as a roadmap, enabling accountants to:

1. Create a reliable, efficient, and standardized process.

2. Break down complex tasks into manageable steps.

3. Improve organization, accuracy, and consistency.

4. Ensure compliance with regulatory requirements.

5. Guarantee the completeness of their work.

6. Reduce year-end stress.

By following a checklist, accountants can streamline their workflow, ensuring that no critical steps are overlooked. This not only enhances efficiency but also minimizes the risk of errors. Additionally, a standardized process promotes consistency across clients, instilling confidence in the accuracy and reliability of the accountant’s work.

Moreover, the checklist acts as a safeguard against regulatory non-compliance. By systematically addressing each regulatory requirement, accountants can avoid penalties and legal issues. This adherence to compliance standards not only protects the accountant but also strengthens the financial integrity of their clients’ businesses.

Furthermore, the checklist fosters a proactive approach to year-end accounting. By breaking down tasks into bite-sized chunks, accountants can tackle them methodically, reducing the likelihood of feeling overwhelmed. This systematic approach not only enhances productivity but also alleviates the stress associated with year-end deadlines.

In essence, a year-end accounting checklist is more than just a tool – it’s a lifeline for accountants navigating the complexities of year-end accounting. By providing structure, organization, and guidance, it empowers accountants to efficiently manage their workload, ensure accuracy, and uphold regulatory compliance. Ultimately, it enables them to deliver exceptional service to their clients while minimizing stress and maximizing productivity.

Reference ; https://contentsnare.com/year-end-accounting-checklist/

However, despite its significance, year-end financial management comes with its fair share of challenges:

1. Missing Receipts and Invoices: Tracking down elusive paperwork can feel like navigating a maze, especially as deadlines loom. Ensuring that all financial transactions are documented and accounted for is essential for compliance and accuracy.

2. Human Error: Despite technological advancements, human error remains a persistent threat in financial management. From typos to calculation mistakes, even minor inaccuracies can have significant repercussions for the business.

3. Manual Data Entry: Relying solely on manual data entry is not only time-consuming but also prone to errors. The risk of misinterpretations, omissions, and inconsistencies looms large, leading to discrepancies in financial records.

4. Inefficient Communication: Effective communication is the linchpin of successful financial management. However, miscommunication among team members can lead to confusion and delays, hampering the year-end closing process.

Reference Book; Title: Standards, Rules & Regulations – Cost Accounting Standards Board

To overcome these challenges, businesses can adopt a systematic approach with a comprehensive year-end financial management checklist:

Reference: https://www.highradius.com/resources/Blog/year-end-accounting-checklist/

1. Prepare a Closing Schedule: Establishing a clear timeline for the year-end closing process is paramount. This schedule should delineate key milestones, deadlines, and responsibilities to ensure a smooth and efficient process.

2. Gather Outstanding Invoices & Receipts: Thoroughly collecting any outstanding invoices and receipts is crucial for completeness and accuracy. This step ensures that all financial transactions are properly documented and accounted for.

3. Review Asset Accounts: Conducting a comprehensive review of asset accounts is essential to verify their accuracy and valuation. This includes assessing both tangible assets, such as equipment and property, and intangible assets, such as patents and trademarks.

4. Reconcile All Transactions: Reconciliation is the cornerstone of accurate financial reporting. Comparing financial records with external sources, such as bank statements and vendor invoices, helps identify discrepancies and ensure data integrity.

5. Accrue Accounts Receivable: Accruing accounts receivable involves recording revenue that has been earned but not yet received. This step ensures that financial statements reflect the true financial position of the business, even if payment has not been received.

6. Accrue Accounts Payable: Similarly, accruing accounts payable involves recording expenses that have been incurred but not yet paid. This step ensures that all financial obligations are accounted for and reflected in the financial statements.

In addition to following this checklist, businesses can leverage technology to streamline the year-end financial management process:

Accounting Software: Investing in robust accounting software can automate routine tasks, such as data entry and reconciliation, reducing errors and saving time.

Task Management Tools: Utilizing task management platforms can help assign and track tasks related to the year-end closing process, ensuring deadlines are met and responsibilities are fulfilled.

Document Collection Tools: Implementing document collection tools can facilitate the gathering and organization of financial documents, streamlining data collection and reducing errors.

Reference Blog: https://www.personalfn.com/dwl/Financial-Planning/financial-checklist-to-keep-in-mind-when-approaching-the-year-2023

In summary, mastering year-end financial management requires meticulous planning, attention to detail, and effective communication. By following a structured checklist and leveraging technology, businesses can navigate the year-end closing process with confidence and ease. The result? Accurate financial statements provide valuable insights and set the stage for success in the year ahead. So, roll up your sleeves, embrace the challenge, and embark on your journey to financial preparedness. Your business will thank you for it!