What is mobile money banking?

Mobile money banking allows individuals to handle financial transactions without visiting a bank branch. Instead, they use their mobile phones to request money by texting a password. Afterward, a bank agent delivers the cash to their location. This banking method is essential in rural Kenyan villages where bank branches are scarce.

How does it work?

In the early 2000s, Kenya pioneered mobile banking, surpassing traditional payment systems in the US. This system doesn’t require a bank account; instead, agents facilitate transactions. These agents function like ATMs, enabling users to deposit or withdraw cash using their mobile money applications. The widespread adoption of mobile money systems has contributed to significant economic growth, particularly in Africa. In Kenya, 72% of the population has a mobile money account, while in Uganda, the figure stands at 43%.

World’s Largest Mobile Pay Network… Is in Kenya

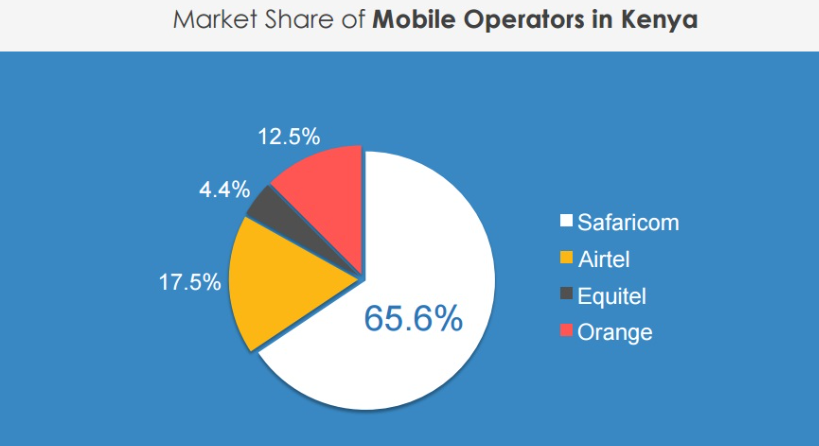

The Kenyan mobile money market as of the present time:

In Kenya, Safaricom’s M-Pesa dominates the mobile money market, despite the presence of other providers like Airtel Money, Orange Money, and Essar yuCash. Within just four years of its launch, mobile money services have seen remarkable growth, with the number of agent outlets skyrocketing from 1072 branches to 46,000. This expansion is primarily driven by Safaricom’s M-Pesa and Equity Bank, supported by favorable regulations, technological advancements, and innovative business models, especially in the mobile phone sector.

Source: Communication Authority of Kenya

The government of Kenya is actively promoting the use of mobile money and has initiated five programs through the ICT board. These programs focus on local digital content, digital inclusion, government applications, business process outsourcing, and

IT shared services. With such initiatives and the growing market demand, the mobile money sector in Kenya is poised for further expansion and development.

What is M-Pesa?

Safaricom, one of Kenya’s leading mobile phone operators, introduced M-Pesa in 2007. This mobile banking service revolutionized access to financial services for Kenya’s population. M-Pesa allows users to transfer and store money using their mobile phones, providing a convenient alternative to traditional banking. The name “M-Pesa” combines “M” for mobile and “Pesa,” which means payment or money in Swahili, reflecting its focus on mobile payments and financial transactions.

Source: Kenyavibe

How Does M-Pesa Work?

M-Pesa operates as a virtual banking system, providing transactional services through a SIM card. Users can initiate money transfers and payments via SMS messages after inserting the SIM card into their phone’s slot. What sets M-Pesa apart is its accessibility: even without a bank account, individuals can utilize numerous M-Pesa outlets distributed across Kenya.

At these outlets, users can hand cash to kiosk attendants, who then digitally transfer the corresponding amount to the user’s M-Pesa account. Conversely, cash withdrawn from M-Pesa can be easily deposited into Safaricom-held bank accounts, which function as regular checking accounts and are insured up to $1000 (or 100,000 shillings) by the Deposit Protection Fund.

For transaction verification, M-Pesa issues receipts. During a transaction, both parties exchange phone numbers, which serve as account numbers. Once the transaction is completed, both parties receive an SMS notification detailing the amount transferred or deposited, along with the full name of the other party. These mobile receipts are received within seconds, promoting transparency and accountability for all parties involved in the transaction.

Mobile Money offers several benefits:

- Speed, Ease, and Affordability: Mobile Money transactions are faster, easier, and often cheaper compared to traditional banking methods. Users can send and receive money with just a few taps on their mobile phones, eliminating the need for physical visits to banks or filling out extensive paperwork.

- Reduction in Paperwork: With Mobile Money, the need for cumbersome paperwork is greatly reduced. Users can complete transactions digitally, minimizing the paperwork associated with traditional banking processes, which leads to increased efficiency and convenience.

- Convenience for Beneficiaries: Mobile Money provides a convenient option for beneficiaries, especially in areas where access to traditional banking services is limited. Users can access their funds anytime, anywhere, making it easier to manage finances and meet their needs.

- Promotion of Service Uptake: Mobile Money helps promote the uptake of various services, including financial services, by providing a convenient and accessible platform for transactions. This fosters financial inclusion by reaching individuals who may not have had access to formal banking services before.

- Profitable Business Opportunity: Becoming a Mobile Money agent can be a profitable business venture. Agents facilitate transactions between users and the Mobile Money service provider, earning commissions for their services. This creates opportunities for entrepreneurship and income generation, particularly in underserved areas where traditional banking infrastructure is lacking.

- Overall, Mobile Money offers numerous advantages that contribute to financial inclusion, economic development, and convenience for users and businesses alike.

Mobile Money also faces several challenges:

1. Platform Integration: Integrating Mobile Money platforms with existing financial systems and technologies can be complex, requiring coordination among various stakeholders and overcoming interoperability issues.

2. Remote Mobile Network Coverage: In remote or rural areas, mobile network coverage may be limited or unreliable, hindering users’ ability to access Mobile Money services.

3. Ensuring Agent Liquidity: Mobile Money agents need to have sufficient liquidity to fulfill cash-in and cash-out transactions. Maintaining adequate liquidity can be challenging, particularly in areas with fluctuating demand.

4. National ID Requirement: Not all recipients may have a national identification document, which is often required for registration and verification purposes. This can exclude certain individuals from accessing Mobile Money services, limiting financial inclusion.

5. Training for New Users: Many users may be unfamiliar with Mobile Money systems and require training to understand how to use them effectively and securely. Providing comprehensive training programs can be resource-intensive.

6. Obtaining Signed Receipts: Traditional banking transactions often involve signed receipts for accountability and security purposes. In the Mobile Money context, obtaining signed receipts for transactions can be challenging, potentially leading to disputes or issues with transaction verification.

7. Recourse for Mistake Payments: Addressing mistakes or errors in Mobile Money transactions can be complicated, especially in cases where funds are sent to the wrong recipient or transactions are processed incorrectly. Establishing clear recourse mechanisms for resolving such issues is essential to maintain user trust and confidence in the system.

Addressing these challenges requires collaboration among Mobile Money providers, regulators, financial institutions, and other stakeholders to develop innovative solutions and ensure the continued growth and effectiveness of Mobile Money services.