Social media negatively impacts self-esteem, financial well-being, and economic standing. A new term, “money dysmorphia,” describes distorted financial views, affecting 29% of Americans, often due to comparing financial situations to others.

Social media platforms like Instagram are causing “money dysmorphia” among Gen Z and millennials, who feel economically inadequate due to their lifestyles not mirroring those of influencers. This perception ignores the fact that many consumers struggle to cover essential costs.

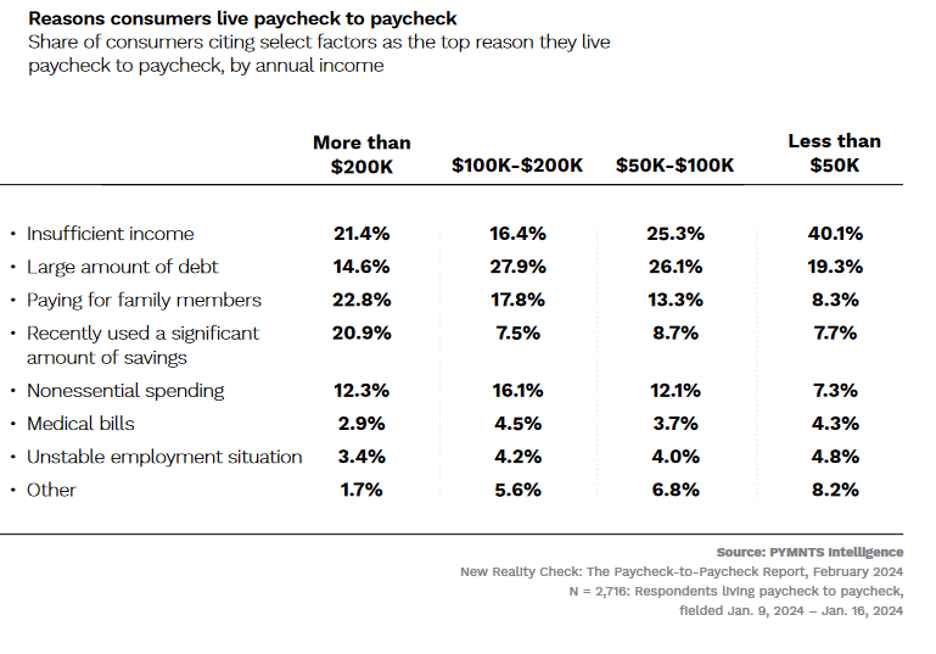

Concurring to the most recent version of PYMNTS Intelligence’s Paycheck-to-Paycheck Report:

“Why One-Third of Tall Workers Live Paycheck to Paycheck,” 62% of U.S. shoppers live paycheck to paycheck, counting more than one-third of those with yearly earnings that surpass $200,000.

The report, which draws on bits of knowledge from a January 2024 overview of 4,285 U.S. customers, found that 53% of infant boomers and seniors presently live paycheck to paycheck, whereas 62% of Gen X respondents do so as well. The rates climb from there as outstanding offers of bridge millennials (68%), millennials (71%), and Gen Z (67%) all report living from one paycheck to another.

Around three-quarters of low-income respondents (those who make less than $50,000 per year) and generally two-thirds of middle-income buyers (those winning between $50,000 and $100,000 every year) say they live paycheck to paycheck.

But indeed higher livelihoods do not show up to immunize a few customers from money-related weights. Forty-eight percent of high-income workers (those yearly winning more than $100,000) say they live paycheck to paycheck, and, inside that rate, there’s a subset of 36% of buyers who win more than $200,000 each year and still live.

High-income earners struggle to manage their money and live within their budgets, with family expenses and nonessential spending being the main reasons they live paycheck to paycheck. They also tap into their savings more than any other income bracket. Affluent consumers allocate a smaller fraction of their budgets to housing and almost one-third to nonessential purchases.

Low-income earners spend less on discretionary items and more on housing and groceries, while high-income earners allocate only 38% of their budgets to these items.

Recent inflation increases may cause financial stress, particularly for high-income earners who may lack disciplined habits to offset their perceived financial woes.

Payments. (2024, March 18). Is social media to blame for perceived financial angst? PYMNTS.com. https://www.pymnts.com/personal-finance/2024/is-social-media-to-blame-for-perceived-financial-angst/